What is operating period in accounting?

1. Definition of operating period

Operating period (also called operating cycle) is the cycle of business activity in which cash is used to buy resources that are converted into products or services and then are sold for cash.

An operating period can be calculated using the following formula:

Operating Period = Average Age of Inventories + Average Collection Period |

Another formula that can be applied in the calculation of an operating period is as follows:

Operating Period = DIO + DSO - DPO |

DIO – Days Inventory Outstanding

DSO – Days Sales Outstanding

DPO – Days Payables Outstanding

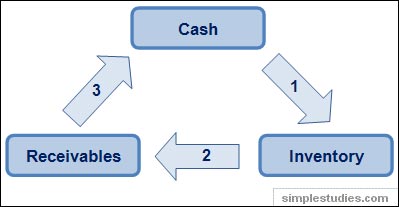

An operating period includes three steps as shown in the illustration below:

Illustration 1: Operating period

At Step 1 a manufacturing company purchases inventory, and therefore, it uses cash. After inventory in the form of raw materials is purchased, it is used in production to become work-in-process and then finished goods as production is completed. If we talk about a retailer, the production process is absent and this step only includes purchase of inventory for a later resale.

At Step 2 a company sells inventory, usually on account (i.e. credit sales). Thus, inventory is converted into accounts receivable. Naturally, some companies sell inventory for cash, and thus, this step is absent for them.

At Step 3 a company collects cash from customers or, in other words, the company collects accounts receivable. This is when the cash finally returns to the company. This step completes an operating cycle.

online accounting course: